Education has long been promoted as the most reliable route to financial security. Society assumes that degrees lead to stable employment, respectable income, and a comfortable life. Parents invest heavily in education with the expectation that their children will never struggle financially. Yet reality tells a very different story. Across countries and cultures, many highly educated individuals live under constant financial pressure, burdened by debt and unable to build lasting wealth.

This paradox exists because education improves earning ability but does not guarantee financial wisdom. In fact, modern educated lifestyles often encourage spending behaviours and mental patterns that quietly weaken financial foundations. Easy access to credit, digital temptations, social pressure, emotional obligations, family expectations, and poor money management habits all play a role.

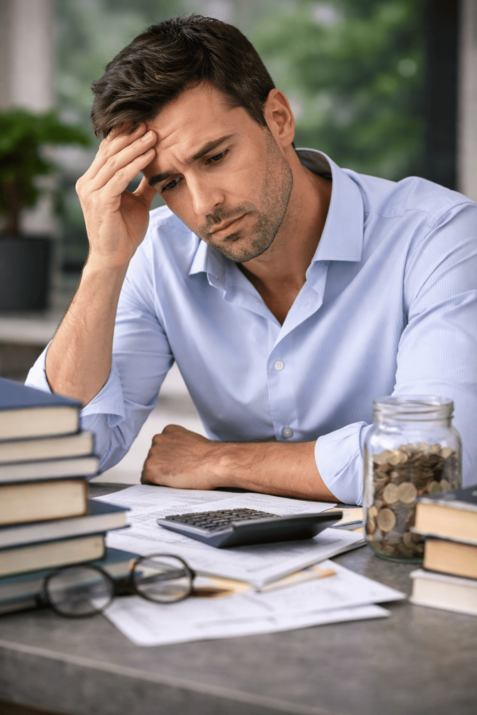

The real question, therefore, is not whether educated people earn money, but why they fail to keep it. The answer lies in daily choices, unplanned spending, wasted time, fear-driven decisions, and the absence of disciplined financial and personal growth systems.

Credit Cards, Digital Spending, and Lack of Financial Planning

One of the biggest reasons educated people remain poor is excessive dependence on credit cards. Credit cards create an illusion of affordability and comfort. Educated professionals, confident in their monthly salaries, spend freely—believing repayment will always be manageable. However, high interest rates quietly eat into income, and over time, a significant portion of earnings goes towards servicing debt rather than building assets.

Unplanned shopping further accelerates this problem. Many educated individuals shop emotionally—buying clothes, gadgets, household items, and online deals without a clear purpose or budget. Discounts and sales trigger impulse purchases, even when the items are unnecessary. Shopping becomes a form of stress relief rather than a calculated decision, leading to cluttered homes and drained bank accounts.

Another major financial leak is online subscriptions and digital spending. Streaming platforms, premium apps, cloud storage, fitness programmes, gaming services, and entertainment memberships operate through automatic payments. Because these expenses are fragmented, they often go unnoticed. Collectively, they reduce saving capacity month after month without delivering proportional value.

Money spent on pleasure-driven websites worsens the situation further. Online gaming, fantasy sports, betting platforms, speculative trading apps, and adult entertainment offer instant gratification but no long-term financial return. Educated individuals often justify this spending as relaxation, yet it silently consumes both time and money.

Perhaps the most damaging factor is the absence of a monthly budget. Many educated people earn regularly but never track expenses. Without a budget, money flows out unconsciously. There is no clear allocation for savings, investments, emergencies, or future goals. Income is consumed by lifestyle habits, leaving nothing behind. In such a system, even high salaries fail to create wealth.

Family Pressure, Siblings’ Financial Dependence, and Emotional Drain

- Another critical reason educated people struggle financially is emotional and social pressure within families.

- Many educated individuals provide continuous financial support to siblings.

- Loans are given for education, marriage, business, or emergencies, often without clear repayment terms. In many cases, this money is never returned.

While supporting family is admirable, repeated financial assistance without accountability weakens one’s own financial foundation. Worse, when the educated individual faces difficulty, the same siblings may be unwilling or unable to help. Emotional attachment replaces financial logic, resulting in long-term financial imbalance.

Lack of family planning also contributes significantly to financial stress. Many educated people do not plan the number of children, education costs, healthcare expenses, or long-term responsibilities realistically. Expenses multiply faster than income, creating continuous pressure. Without planning, even good earnings feel insufficient.

Pampered children add another layer of strain. Parents often fulfil every demand—latest gadgets, branded clothes, expensive schools, frequent outings, and luxury experiences. Children grow accustomed to instant gratification, while parents sacrifice savings, investments, and retirement security to maintain appearances or avoid guilt.

Lack of family planning also contributes significantly to financial stress. Many educated people do not plan the number of children, education costs, healthcare expenses, or long-term responsibilities realistically. Expenses multiply faster than income, creating continuous pressure. Without planning, even good earnings feel insufficient.

Career Stagnation, Laziness, and Wasted Free Time